Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

February 9, 2025

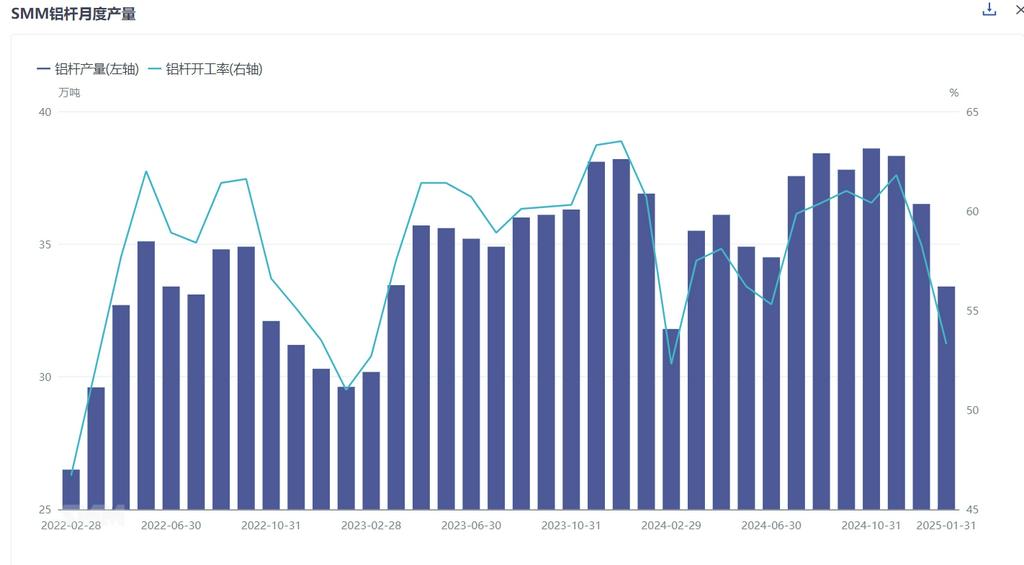

According to the latest monthly survey by SMM,the total aluminum rod production in China in January 2025 was 334,100 mt, down 31,000 mt MoM compared to December. The operating rate of manufacturers recorded 53.34%, a MoM decrease of 4.95%. Compared to January 2024, aluminum rod production decreased by 30,900 mt, and the operating rate of manufacturers dropped 4.75% YoY. The significant YoY decline was mainly due to the earlier Chinese New Year holiday this year, leading to earlier production cuts and holiday breaks, which caused both production and operating rates to fall.

By region, the reduction in aluminum rod supply was notable in January.In Shandong, a major hub for aluminum rod production, the operating rate of local manufacturers fell by 4.61%, while in Henan, the operating rate dropped by 4.67%, showing similar declines. Additionally, Shanxi and Ningxia experienced significant production cuts due to post-holiday inventory pressure, with operating rate declines exceeding 20% in both regions. Meanwhile, operating rates in Yunnan, Guizhou, and Guangxi also further decreased. However,manufacturers in Inner Mongolia and Qinghai saw a countertrend increase in operating rates,mainly due to the high pressure to consume liquid aluminum during the holiday, maintaining production rhythm with slight increases.

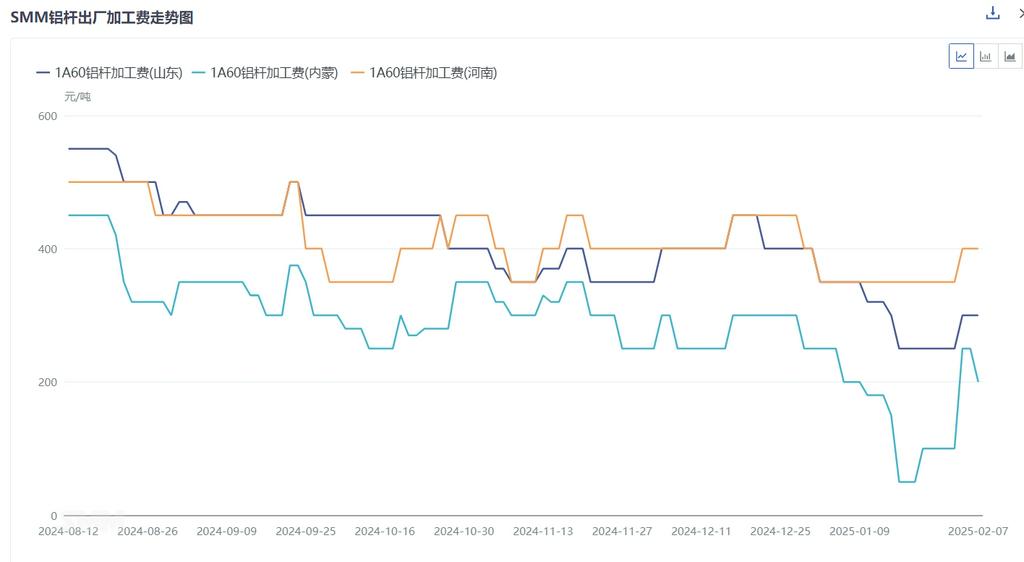

Regarding specific processing fees, in January, the ex-factory monthly average price of 1A60 processing fees in Shandong was 297 yuan/mt, down 107 yuan/mt MoM; in Henan, the ex-factory monthly average price was 350 yuan/mt, down 70 yuan/mt MoM; in Inner Mongolia, the ex-factory monthly average price was 150 yuan/mt, down 125 yuan/mt. Among the three major trading regions, the delivered monthly average price in Hebei was 319 yuan/mt, down 108 yuan/mt; in Jiangsu, the delivered monthly average price was 420 yuan/mt, down 107 yuan/mt; and in Guangdong, the delivered monthly average price was 488 yuan/mt, down 71 yuan/mt.

In the segmented market,the demand for ordinary rods has clearly entered the off-season,with increasing inventory accumulation risks at factories, reflected in processing fees. For high-conductivity aluminum rods, the current ultra-high voltage orders have temporarily ended,but as market suppliers remain limited, despite price risks, overall processing fees are still at a relatively high level. For example, the ex-factory price in Shandong is reported at 600-1,000 yuan/mt, with relatively ample profit margins. For aluminum alloy rods, nearing the year-end in January,new energy grid connection orders showed weak performance according to enterprise feedback. For enamelled wire aluminum rods,related orders in January also declined in activity due to seasonal factors, with a cooling in order performance.

With 2024 behind us, how will the aluminum rod market perform in 2025? On the demand side, although power grid investment in 2025 is expected to exceed 650 billion yuan, there is at least a three-month time lag from bidding to review and announcement for power grid orders. Based on current feedback from downstream aluminum wire and cable enterprises,the State Grid's delivery volume in Q1 is not as strong as the same period last year. Therefore, even though downstream has resumed work, stockpiling sentiment may remain pessimistic. On the supply side,the aluminum rod industry is currently influenced by factors such as aluminum liquid alloying and intense competition in aluminum billet processing fees, leading to a gradual increase in operating capacity. It is understood that new capacities in Xinjiang and Guizhou are expected to come online this year, potentially intensifying competition in the aluminum rod market. SMM believes that as downstream resumes work after the holiday while supply reductions remain limited, the supply side will lean towards looseness, and aluminum rod processing fees are expected to face downward pressure.

For queries, please contact William Gu at williamgu@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn